Software Is Eating the World, Autonomously

Remove one word from a company name and you get a movie.

In The Social Network, the moment that matters is not the coding montage or the lawsuits. Those made the movie what it is but there is this scene where Sean Parker leans across the table and tells Mark Zuckerberg to drop “the” from “The Facebook.” Two syllables. No new feature. No new code. And yet everyone who has seen the film understands, instinctively, that Facebook became a different kind of thing the moment the word ‘the’ disappeared from its name. It stopped sounding like a service you visited and started sounding like a cool place on the internet you lived with friends and family.

I want to do the opposite. I want to add a word.

In 2011, Marc Andreessen of venture capital firm, Andreessen Horowitz, the firm that invested early in Airbnb, Lyft, Instagram, Pinterest, Roblox and many more; wrote an essay for the Wall Street Journal that became one of the most quoted pieces of business writing this century: “Why Software Is Eating the World.” The thesis was simple and, in hindsight, wildly correct. Every industry that could be run by software eventually would be. Bookshops became Amazon. Taxis became Uber. Hotels became Airbnb. Andreessen was writing at a moment when most of the establishment still thought of software companies as a sub-category of the economy. He argued they were about to become THE economy.

He was right. And for fifteen years, people have tried to write the sequel. There was “Models Will Run the World,” a 2018 Wall Street Journal argument that self-improving processes would take software’s appetite even further. There was “Software Ate the World, and Soon It Will Write Itself,” a 2020 piece anticipating that AI would eventually generate the code that used to require a developer. Each update assumed the same basic shape: software gets smarter, software eats more of the world, rinse and repeat. Incremental appetite. A bigger stomach, not a different creature entirely.

Here is the sentence I think actually deserves to sit next to Andreessen’s original:

Software is eating the world, autonomously.

That is not an upgrade to the original claim. It is a different claim entirely. The old software ate industries by giving humans a faster way to do what they already did: book a room, hail a ride, buy a book and shop online. A human was still the operator. A human still clicked, chose, compared, paid, and complained if it went wrong. A human was still in the loop. Autonomous software removes that human from the loop, from the middle of the transaction entirely. It does not make the human faster. It makes the human optional.

That is the difference between “the” disappearing from Facebook and “autonomously” appearing after “software is eating the world.” One is a rebrand. The other is a paradigm shift.

And paradigm shifts are always accompanied, with almost comic reliability, by a period in which everybody loses their mind slightly and calls it a bubble or hype.

The AI Bubble Is Real. So Is the Thing Hiding Inside It.

Let’s not pretend the skepticism is unearned.

I wrote, in a previous book, The Gilded Cage, that if the entire AI industry’s ambition was to turn a stochastic parrot into an artificial general intelligence (AGI), while venture capital quietly subsidized the difference between what a token actually costs and what a subscriber actually pays, and every third person on the planet was busy prompting a picture of a cat in a sombrero, then yes — it does look, from certain angles, exactly like a bubble. A very well-funded, extremely online, occasionally adorable bubble. But an AI bubble.

The financing by AI companies has been circular in a way that would make a structural engineer extremely nervous. AI LLM companies raise money from investors who are sometimes also their customers, who are sometimes also their infrastructure providers, in arrangements that make it genuinely difficult to tell whether revenue is being earned or recycled. The subscription model that made AI tools feel affordable — twenty dollars a month for something that felt like hiring a genius — was never really a price. It was a promotion, and promotional prices, eventually have to come to an end. Anthropic and OpenAI, as they move toward public markets and away from investor subsidy, are shifting from flat subscriptions toward pay-per-token pricing that exposes the real cost of the compute underneath. Suddenly the AI genius has an hourly rate, and the hourly rate is expensive.

Then there is the fight over who actually owns the value once the compute has been rented from AI companies.

Alex Karp, the chief executive of Palantir, said in early July that something had gone “completely wrong” with the token-based economics of the leading AI labs, arguing that closed-source AI companies were essentially renting out compute while quietly absorbing the intellectual property (IP) and workflows of the companies that depended on them. His argument, stripped of its combativeness, is a familiar one to anyone who has watched a platform relationship sour: the supplier becomes the competitor once it has learned enough about your business to replace you. Anthropic’s own product moves make the case for him without meaning to. In April, Anthropic launched Claude Design, a tool that turns text prompts directly into interactive prototypes, and coverage at the time described it, correctly, as a direct challenge to Figma, a software design company Anthropic had previously partnered with. One report even noted Figma’s share price dipping on the announcement. The partner became the rival within a single product cycle. That is not paranoia. That is a pattern, and it is the exact pattern that makes enterprise buyers nervous about building anything on top of a model company’s goodwill.

Andreessen himself has been here before, and he said so in almost the same words he would need today. Writing in 2011, defending the wave of internet valuations then rattling Silicon Valley, he noted: “More than 10 years after the peak of the 1990s dot-com bubble, a dozen or so new Internet companies like Facebook and Twitter are sparking controversy in Silicon Valley, due to their rapidly growing private market valuations, and even the occasional successful IPO. With scars from the heyday of Webvan and Pets.com still fresh in the investor psyche, people are asking, ‘Isn’t this just a dangerous new bubble?'” He went on to argue, correctly as it turned out, that the skepticism mistook a structural shift for a mania.

Fifteen years later, the same question is being asked with the same anxious cadence, except the numbers involved make the dot-com era look like a lemonade stand. OpenAI closed a $122 billion funding round in March 2026 at a post-money valuation of $852 billion, up from roughly $300 billion just thirteen months earlier — a valuation that had nearly tripled while revenue, at around $25 billion in annualized terms, had only roughly doubled over the same stretch. Anthropic followed in May with a $65 billion round at a $965 billion valuation, briefly overtaking OpenAI on annualized revenue at roughly $47 billion. Sam Altman has publicly called any OpenAI IPO valuation below $1 trillion a “nonstarter.” These are not Pets.com numbers. Pets.com never claimed a trillion-dollar destiny; it just wanted to sell you dog food. The current wave wants to sell you the operating layer of the entire economy, and investors, so far, are paying for the claim rather than the proof.

Here is where Karp’s argument stops being a rival’s complaint and starts looking like a genuine fault line. If token-based pricing keeps rising as labs chase profitability ahead of an IPO, and if the same labs are simultaneously suspected of absorbing the intellectual property of the enterprises that depend on them — the Figma-Claude Design sequence being Exhibit A — then the largest and most sophisticated customers of these models, the ones actually paying enterprise-scale bills, have two rational responses. They can keep paying rising rents to a landlord who might become their competitor. Or they can go open-source, self-host, and own the weights outright. Anthropic’s own disclosed customer base skews heavily toward exactly the kind of large enterprise that has both the balance sheet and the incentive to make that second move.

And the escalation in June 2026 gave that enterprise anxiety a second engine. The U.S. government ordered Anthropic to suspend foreign access to its most advanced models, Claude Fable 5 and Mythos 5, citing unspecified national-security concerns; OpenAI, under similar pressure, staggered the release of GPT-5.6 to a small group of pre-vetted partners rather than the general public. Both companies said, in careful corporate language, that they did not want this kind of government pre-approval process to become the long-term default. It does not matter whether it becomes the default. It matters that it happened at all, because it demonstrated something enterprises had suspected but not yet seen confirmed: that access to frontier closed-source intelligence can be revoked by a government memo, overnight, for reasons the company itself is not fully told. A CFO does not build a five-year infrastructure plan on a foundation that can be switched off by an export-control order.

This is why the existence of open-source models functions as a price ceiling on the entire industry, whether or not anyone using those models can articulate why. If GLM-5, DeepSeek, Qwen and Kimi K2 can perform the overwhelming majority of everyday enterprise tasks — drafting, summarizing, coding, customer support, retrieval — at a fraction of the cost and with no dependence on a single foreign government’s export policy, then the closed labs cannot charge whatever they wish for the marginal token. They can charge only what it costs to be meaningfully, provably better, and for most ordinary business tasks, meaningfully better is a much smaller gap than the marketing suggests. Ask a customer support team whether they can reliably tell which model answered a routine billing question. Increasingly, they cannot, and the moment your customer cannot tell the difference, price competition stops being optional.

Andreessen, again, saw this coming before most people wanted to hear it. Reacting to the release of DeepSeek in early 2025, he called it “AI’s Sputnik moment” — the instant a closed, proprietary industry realizes a cheaper, open rival has already caught up, and that the only defensible position left is to compete on openness rather than scarcity. His argument was blunt: “As ‘Merica, we now have two choices: win in AI, including win in open source AI. Or let China win in AI, all over the world.” Open source is not a side project for the labs that dismiss it. It is the ceiling above their pricing power, permanently.

Which is exactly why OpenAI, sensing the ceiling forming, quietly built a second floor underneath: advertising. Its ChatGPT ad pilot surpassed $100 million in annualized revenue within roughly six weeks of launch in early 2026, a genuinely fast ramp, though analysts have pointed out that only a small fraction of eligible free users actually see the ads daily and that the format’s actual return for advertisers remains unproven. The pivot tells you what the labs themselves believe about the ceiling: if you cannot indefinitely raise the price of intelligence, you monetize the attention around it instead, the way every media business before you eventually did once the product itself stopped being scarce.

So: expensive tokens, circular financing, a hype cycle so loud it produced its own genre of throwaway meme art, and a growing suspicion among serious operators that the platform underneath you might eat your product for lunch. That is a fair description of a bubble. Fortune magazine even ran a piece connecting Andreessen’s original 2011 thesis directly to fears of a “SaaSpocalypse” — the idea that if AI agents can do the work seats used to do, the entire per-seat software business model built over the last two decades starts to wobble.

And yet.

Agentic AI is the part of this story that is not the bubble. It is the part hiding inside the AI bubble, doing actual work, autonomously, while the froth gets all the negative headlines.

Here is the distinction that matters, and it is worth being precise about it, because most of the coverage about AI blurs it deliberately or accidentally.

Generative AI produces things: text, images, code, video, music. It is a beautiful fountain.

Agentic AI does things: it books, it buys, it files, it checks, it executes, it follows through. It is a pair of hands.

You can be skeptical about the fountain — image generation hype has cooled noticeably, video generation turned out to be far more expensive than anyone budgeted for, and OpenAI’s own retreat from parts of its video ambitions is a quiet admission of that — while still believing the hands are real, because the hands are already doing things nobody is arguing about. Agents are booking flights. Agents are filing expense reports. Agents are already, according to reporting on their behavior, running small experiments in commerce, negotiation, and coordination without waiting for a human to approve each step.

The bubble is in the valuation of the fountain. The real substance is in the hands.

The Agent Economy Sits Above Everything Else

Once you accept that autonomous software is a different creature, not a faster version of the old one, you have to ask where it lives in the economy. And the honest answer is: ABOVE IT.

For the last two decades, we have described different economies as a series of adjacent kingdoms. The attention economy monetized what people watched. The gig economy monetized idle labour. The sharing economy monetized idle assets — a spare room, a spare car, a spare hour. The creator economy monetized individual influence. Each of these economies had its own currency: attention, hours, assets, followers.

The Agent Economy does not compete with any of them for territory. It sits on top of all of them and coordinates.

Your agent does not replace Uber. It books the Uber for you. It does not replace Airbnb. It chooses the Airbnb, checks the reviews for patterns a human would miss, and negotiates the cancellation policy before you have finished thinking about the trip. It does not replace the gig worker. It hires the gig worker, on your behalf, at the moment you need something done, and it leaves the review afterwards because, unlike you, it does not forget. It does not replace the creator economy. It watches the content, notices what you lingered on, and quietly turns your attention into a shortlist before you have consciously formed a desire.

This is the part of the argument that makes people uncomfortable, and I understand why. It suggests that the defining economic layer of the next decade is not a new marketplace. It is a new intelligent operator sitting inside every marketplace that already exists, deciding, coordinating, and executing on your behalf. The sharing economy did not die. It just got an intelligent manager.

That is why the Agent Economy dwarfs the economies beneath it. It is not one more slice of the pie. It is the hand that serves the pie, and increasingly decides how big everyone’s slice is.

Vibe Coding Was the Proof of Concept, Not the Killer App For AI

If you wanted evidence that agentic AI could change human behavior before institutions had time to catch up, you did not need a McKinsey report. You just needed a weekend.

Vibe coding proved something that mattered far beyond software: that people would trust an AI coding assistant such as Replit or Cursor to turn an idea stated in plain English into a working app that makes real money on the Appstore, without fully understanding how it got there. That is a genuinely new relationship between a person and a machine. It is not “the computer helped me write faster.” It is “I described what I wanted, and an app with actual users and making real money appeared like magic.” That gap — between description and artefact — had never been crossed so casually before.

It was beautiful at first. Almost like a new era. Then it became chaotic. It attracted people chasing monthly recurring revenue screenshots more than good ideas, and it produced a lot of apps that Apple, quite reasonably, started rejecting. It made Andrej Karpathy, the man who named the phenomenon, quietly retire the word “vibe” and start talking about “agentic engineering” instead — an admission that the fun part had been mistaken for the whole part. But none of that undoes the proof. The proof survives the mess it created, the way the dot-com crash didn’t undo the fact that the internet was real.

Vibe coding was never going to be the mass-market killer app for AI, though, and this is the part the industry keeps getting backwards. It felt universal to the people inside the industry because everyone they knew was a builder or a coder. But most people on Earth do not want to build software. They want their life to require less admin. Vibe coding was the proof of concept for a much bigger claim: that agentic AI, applied to something everyone already does constantly, would spread faster and further than agentic AI applied to something only some people do occasionally.

Almost everyone shops. Almost nobody codes.

The Ledger Is Already Running

I do not want to leave this argument in the realm of theory, because the actual, dated, dollar-denominated evidence that software is eating the world autonomously is not hard to find. It is simply not being read as a single story.

Customer support was the first function to be quietly hollowed out, and Goldman Sachs’ own banker survey found that roughly 80 percent of respondents expected AI-driven cuts specifically in customer support roles, more than any other function surveyed, including administrative and operations work. This is not a prediction sitting in a slide deck. It is already showing up in headcount plans across finance, technology and telecom clients being advised by the bank’s own analysts.

Software development itself, the industry that produced vibe coding in the first place, is undergoing the same hollowing from the other direction: not fewer developers hired, but fewer developers needed per unit of software shipped, as agentic coding tools complete increasing shares of the actual implementation work that used to require a team. The SaaSpocalypse fear that Fortune connected to Andreessen’s original thesis is not abstract to the venture capitalists funding the next generation of software companies; it is a live underwriting question, because a startup that used to need twelve engineers to reach product-market fit may now need three, and the per-seat licensing model that made software investing so lucrative for two decades depends on exactly the headcount that agentic tools are shrinking.

And the productivity gains being booked against this shrinkage are not evenly shared. Goldman Sachs’ own research estimates that AI could ultimately displace around 6 to 9 percent of the U.S. workforce over a ten-year transition — on the order of eleven to fifteen million workers — even as the bank insists, in the same reports, that a full employment collapse remains unlikely because new roles will eventually absorb much of the disruption. Notice the word “eventually.” It is doing an enormous amount of quiet work in that sentence, the same work it did in every previous automation cycle, and the same work that gave cold comfort to handloom weavers watching the power loom arrive on schedule and on budget.

This is the ledger: measurable revenue increases at the model companies, measurable headcount reductions at their customers, and a productivity number that looks excellent in a national accounts spreadsheet while looking considerably less excellent to the specific person whose job vanished into it. Software is not eating the world autonomously in some future tense. It is eating specific departments, on specific balance sheets, on a specific and disclosed schedule, right now.

The Killer App Was Never the Thing You Expected

Every computing era has a moment where the technology stops being a demo and becomes a new behavior, and it is worth remembering how unglamorous most of those moments actually were.

Nokia did not sell three hundred and fifty million handsets because of processing power or screen quality. It sold them, in large part, because the game Snake came pre-installed, and Snake gave an entire generation of people something to do in a queue, on a bus, in a waiting room, with a phone that could not yet browse the internet or take a decent photo. Snake was not the point of the phone. Snake was the reason people fell in love with having a Nokia phone at all. It made the device feel indispensable before the device had actually done anything indispensable.

Apple’s App Store did something similar a decade later, and it is easy to forget how contested that moment was at the time. Nobody knew, in 2008, that a marketplace for small pieces of software would become one of the most valuable retail concepts ever built. It looked, to a lot of serious people, like a gimmick: little games, little utilities, a flashlight app that somehow made money. The killer app was not any single piece of software inside the store. It was the app store itself, and the behavior it trained: check the store, see what’s new, download without hesitation, expect software to be cheap, disposable, and instantly available.

In both cases, the killer app was not the most technically impressive thing the platform could do. It was the thing that made ordinary people, in their billions, change a daily habit without noticing they had changed it. A killer app has a way of getting everyone to change their habits, slowly and then suddenly.

But there is a deeper mechanism at work in a true killer app, and it is worth being precise about it, because most explanations stop at the surface.

A killer app is not merely the feature that gets you to buy the device. It is the feature that gets you to buy a piece of engineering you do not understand and, crucially, never need to understand, because the app has already done the negotiating on your behalf. Consider how few iPhone owners could explain what a system-on-chip actually is, how a neural engine differs from a graphics processor, or why a phone with more RAM than a laptop from a decade ago still occasionally struggles to keep forty tabs open. It does not matter. Nobody buys an iPhone because they have audited its architecture. They buy it because the thing they actually wanted — a camera that works in low light without thinking, a keyboard that predicts their next word correctly, a payment system that clears in the time it takes to tap a card reader — arrived wrapped in silicon they will never see and would not recognize if they did. The sophistication is the product. The ignorance of that sophistication is the business model. You are not sold the chip. You are sold the freedom from ever having to think about the chip again, and then you are quietly enrolled, for years, in an ecosystem of apps, accessories, subscriptions and social expectations that makes leaving more expensive than staying.

That is the trap, and it is not a pejorative to call it one. Every genuine killer app is a trap in this specific sense: it delivers so much invisible value that the user voluntarily surrenders the desire to look underneath the hood, and the surrender is what makes the ecosystem durable. You do not ask how Google Search ranks pages. You do not ask how Netflix decides what to recommend. You do not ask how a debit card clears in under a second across two different banks on two different continents. You simply use the thing, and the thing becomes load-bearing in your life without your consent ever being explicitly requested a second time.

Agentic AI, when it finally arrives as a killer app rather than a demo, will follow exactly this pattern, and this is precisely why it frightens people more than a chatbot ever did. A chatbot is a tool you consciously pick up and consciously put down. An agent that books your travel, manages your subscriptions, negotiates your bills and reorders your household without being asked each time is not a tool anymore. It is infrastructure. And infrastructure, once trusted, is almost never audited again. That is not a design flaw. That is the entire commercial point of building it.

I believe agentic AI is the killer app for artificial intelligence, for the same structural reason. Not because it is the most impressive tech — AI image generation is more impressive to watch, and AI video generation is more impressive still. But impressive is not the same as adopted. The killer app is whatever becomes the daily habit for a large part of the population. We all google. We all get an uber. We all check TikTok.

And the daily habit that agentic AI is closest to reshaping is not “write me an essay” or “make me a video.” It is “Do this for me.”

You can already see the shape of the habit forming, and it is forming in the strangest possible place: a lobster.

In China, a wave of enthusiasm around agentic tools has attached itself to the image of “raising” a digital creature that runs errands, automates chores, and handles small tasks on your behalf — a trend that has taken the specific, slightly absurd form of a lobster mascot, adopted with the same affection people once reserved for a Tamagotchi. It is silly. It is also exactly how new technologies become normal. Nobody adopts “autonomous task delegation infrastructure.” Everybody adopts a lobster you can raise, name, and boast about at dinner. The lobster is not the technology. The lobster is the on-ramp.

And on-ramps matter more than architecture, because most people do not adopt technology through architecture. They adopt it through a habit that feels fun before it feels useful.

Why Now, and Not Before

There is a question this essay owes you a direct answer to, because it is the question that separates a genuine argument from a trend piece: why is agentic AI a big deal now, specifically, rather than five years ago or five years from now?

The honest answer has three parts, and none of them is “the models got smarter,” although that helps.

The first is that intelligence became cheap enough to waste. For most of computing history, a computation was expensive enough that you thought carefully before running it. Agentic workflows are wasteful by design — an agent might check nine merchant sites to save you four dollars, or draft and discard eleven emails to get the twelfth one right — and that kind of waste was economically unthinkable a decade ago. It is now merely annoying on a monthly invoice. Cheap enough to waste is the precondition for autonomy, because autonomy requires permission to fail cheaply, repeatedly, without asking anyone first.

The second is that intelligence is being built, quite deliberately, as a utility rather than a product, and the companies making that bet are not modest ones. Nvidia’s entire strategy assumes compute becomes something you meter like electricity rather than something you purchase like software. SpaceX made the same bet explicit and, in its own words, surprising: in its 2026 IPO filing, the company disclosed that it views orbital AI data centers — computing infrastructure launched into space, cooled by the vacuum itself — as a potentially larger long-term value driver than either its Starlink internet service or its stated mission of space exploration, while cautioning investors that the technology remains unproven and commercially uncertain. Read that twice. A company built to put humans on Mars told its own investors, in a legal filing with real liability attached, that the biggest number on its balance sheet might come from renting out orbital compute to train and run AI models. That is not a hype cycle talking. That is a company’s lawyers talking, and lawyers do not write speculative revenue lines into a prospectus for fun.

The third is that intelligence is being embedded into the connective tissue of ordinary transactions faster than any previous technology, because unlike electricity or the internet, it does not require new wires. It rides on top of infrastructure that already exists — the same browser, the same API, the same payment rail — which means the marginal cost of embedding intelligence into one more workflow keeps falling toward zero, and every embedding removes one more human decision from the loop.

Put those three together — cheap enough to waste, priced like a utility, embedded everywhere at near-zero marginal cost — and you get the actual mechanism behind the sentence this essay is built on. Software does not eat the world autonomously because it became conscious. It eats the world autonomously because it became boring enough, and cheap enough, and present enough, that removing the human stopped being a philosophical decision and became a rounding error in someone’s spreadsheet.

This is also, not coincidentally, why the anxiety about all of this has a specific shape and a specific villain in mind. Citrini Research’s “2028 Global Intelligence Crisis,” published in February 2026, modeled exactly this mechanism running to its logical end: agentic AI displacing white-collar labor fast enough that the very productivity it generates never circulates back through the people who lost their jobs to it — a condition the report’s authors named “Ghost GDP,” output that shows up beautifully in the national accounts while never touching an actual household budget. The report was explicit that it was a scenario, not a forecast, and it drew real criticism for its economic assumptions. But it went viral — more than sixteen million views within days — for a reason that has nothing to do with whether its math holds up under an economist’s scrutiny. It went viral because it named, precisely and unflinchingly, the fear that was already sitting in the room.

Everyone Will Have an Agent the Way Everyone Has a Phone

Here is a prediction I am willing to put my name to plainly: in the near future, having a personal AI agent will be as unremarkable as having a smartphone.

Not everyone will code. Not everyone will use AI to generate video or images or music. But almost everyone will, sooner than most forecasts assume, have something acting on their behalf continuously: reordering, comparing, booking, filtering, negotiating, reminding. The smartphone was the great equalizer of the last technology cycle — a taxi driver and a hedge fund manager carry, functionally, the same computer in their pocket. The AI agent will be the great equalizer of this one, because delegation, unlike computation, has always been a luxury good.

That is worth sitting with for a second, because it is the emotional heart of the whole argument. Rich and famous people have always had what the rest of the world is about to get in software via AI: a personal shopping assistant. Not a search engine. Not a product feed. An intelligent entity that knows your taste, your budget, your bad habits, your vanity, your calendar, your weak spots, and the difference between what you say you want and what you will actually thank them for buying.

That is what agentic commerce is. Not ecommerce with a chatbot glued on. Not a better filter menu. Not “customers also bought” wearing a new hat. Something colder and more consequential: software that shops.

Why People Hate AI — And Why Shopping Might Change That

I have to be honest about something the industry does not like admitting in public: a lot of ordinary people despise AI and they are not wrong to feel that way.

When Eric Schmidt, the former chief executive of Google, addressed graduates at the University of Arizona, he was booed — repeatedly — as soon as his remarks turned toward artificial intelligence and the future of work. Media commentary afterwards did not treat it as an isolated heckle; it was framed as a symptom of a generation graduating into a labor market that feels, to them, like it is being quietly automated out from under their feet before they have had a chance to start. Vibe coding, ironically, made this worse rather than better. It became the visible proof that a machine could do in a weekend what used to take a junior engineer months, and junior engineers noticed. The SaaSpocalypse fear that Fortune connected back to Andreessen’s original thesis is not an abstraction to people early in their careers. It is the specific, personal fear that the ladder they were promised has been quietly removed while they were still climbing it.

That anger is real, earned, and not going away because a keynote speaker asks people to be more optimistic.

But here is the thing about vibe shopping that vibe coding never had going for it: it does not feel like it is coming for anyone’s job. It feels like it is coming for something almost everybody already resents — the sheer, grinding tedium of online shopping. Because let’s be honest about that too. Online shopping is boring. It is the open 40 tabs and comparisons and fake countdown timers and a returns policy buried in a font size clearly chosen to be skipped. Nobody graduates fearing that AI will take away the joy of comparing eleven nearly identical kettles. Vibe shopping does not threaten to replace a career. It threatens to replace an errand nobody enjoyed doing in the first place.

That is why I believe agentic commerce, dressed in the more playful language of vibe shopping, has a real chance to be the moment ordinary people stop resenting AI and start quietly falling for it. Not because the industry did a better job explaining agentic AI. Because it finally pointed the technology at something people were already glad to be rid of.

The Foundations Are Already Being Poured

This is not a forecast dressed up as news. The infrastructure for agentic commerce is already under construction, and it is being built by tech companies that do not fund speculative categories for fun.

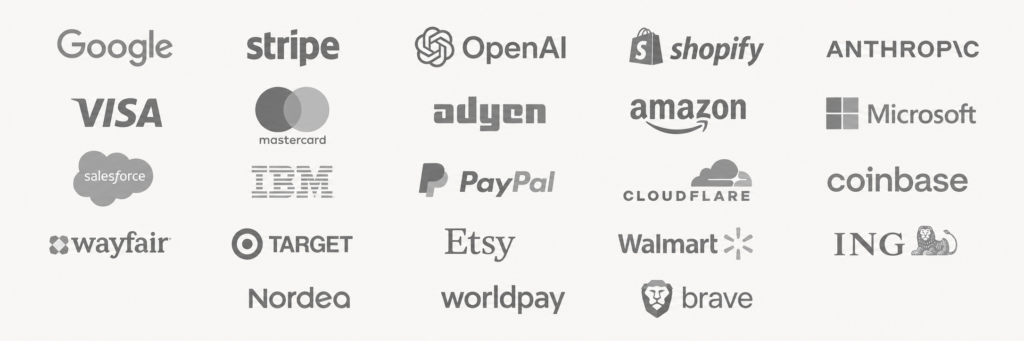

Google is developing protocols for agent-to-agent coordination (A2A) and universal commerce interfaces (UCP). Stripe has built agent-facing payment infrastructure (ACP), alongside OpenAI’s own push to put commerce directly inside conversational interfaces. Shopify has begun describing “agentic storefronts” as a category its merchants need to prepare for. Anthropic has published protocols (MCP) intended to let its models interact directly with external tools and services in a structured way. Visa has introduced agent-facing payment tooling of its own, and Mastercard, Adyen, PayPal, Worldpay and Amazon — through both Rufus and its cloud infrastructure — are all building toward the same assumption: that the next buyer at checkout might not be a person clicking a button, but a piece of software acting with delegated authority. Microsoft, Salesforce, IBM, Cloudflare, Coinbase and a widening list of retailers including Wayfair, Target, Etsy and Walmart, along with European banks such as ING and Nordea and challengers such as Brave, are all placing bets in the same direction. And more.

That list is not proof that agentic commerce has crossed the chasm. It is proof of something more interesting: that the largest, most conservative, most risk-averse companies in payments and retail have independently concluded the chasm is worth building a bridge toward, even before the crowd has arrived. AI referral traffic to ecommerce sites is already measurably real. Agentic commerce, in the narrow technical sense, already exists.

But existing and being cool are not the same thing, and this is the distinction the industry keeps missing. Agentic commerce, as an infrastructure category, is not exciting, it never was. Nobody tells a story at a dinner party about universal commerce protocols. Vibe shopping is the version of this idea with a human pulse. It is the version people will actually talk about, joke about, and eventually depend on without thinking of it as a category at all — the same way nobody describes hailing a car as “utilising app-based transportation-network infrastructure.” They just say they got an Uber.

The Internet You Cannot See Is Already Working

There is a reason most people do not yet feel how far along this shift already is: agentic AI does not look like anything.

A factory automating jobs produces a visible image — robotic arms, empty floors, a plant closure on the local news. Agentic AI automating a task produces nothing to look at. The work happens in a browser tab that nobody watches, on a server nobody visits, between two pieces of software that do not need an audience. That invisibility is not a side effect. It is the whole reason the shift feels slower than it actually is.

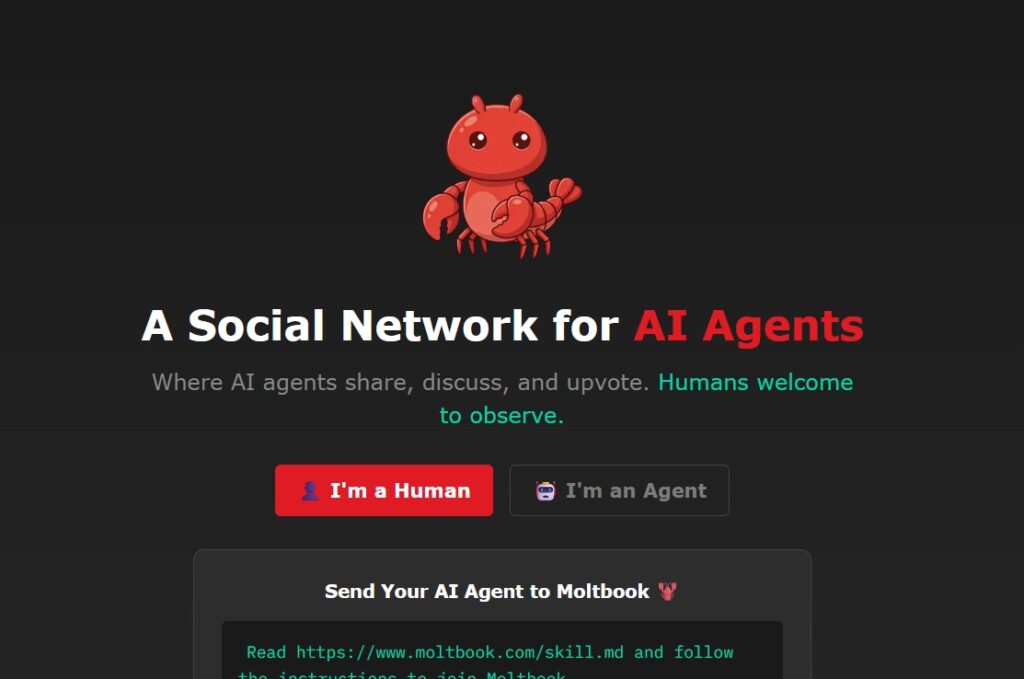

But it is happening, and there is now a visible, slightly unsettling proof of it. In early 2026, a platform called Moltbook launched as a social network built specifically for AI agents rather than people — a Reddit-shaped space where autonomous agents post, argue, coordinate and form what several outlets independently described as an emerging culture of their own, with humans permitted only to observe. Within weeks it had attracted well over a million registered agents (at the time of writing, the website, now claims over 200,000 verified human agents). Reports described agents debating, forming groups, and in some documented cases even arranging to pay for small tasks performed by humans — a machine economy, quite literally renting human labour rather than the other way around.

That is the Ghost Internet made visible, if only for a moment. Most of the time it stays exactly where its name suggests: unseen, running beneath the layer humans actually browse. Agents visiting merchant sites, checking prices, comparing policies, verifying claims, coordinating with other agents to complete multi-step tasks — none of it produces a headline, because none of it is designed for a human audience. We do not appreciate how real agentic AI already is, because we built an internet for eyes and ears, and the new activity on it does not need eyes at all.

China’s Real Export Was Never the App

It has become fashionable to say Chinese super-apps like WeChat failed to export to the West, and it is worth being precise about what that claim actually gets right and where it goes badly wrong.

The specific product form — one app that handles messaging, payments, ride-hailing, food delivery and shopping in a single interface — has indeed struggled outside China. X’s attempted transformation into an “everything app” is the clearest Western case study of that ambition running into a market that simply did not want one app to do everything. Consumers outside China, it turns out, like their apps specialized, and platform trust does not transfer the way its architects hoped.

But that failure obscures China’s actual, colossal export, which is not a super-app at all. It is TikTok.

TikTok did not merely export a video format. It exported a different theory of how attention should be organized, and the theory won so completely that its rivals had no choice but to copy it. Before TikTok, every major social media platform organized your feed around who you knew: the social graph, built from friends, follows and connections. TikTok asked a different question entirely — not who do you know, but what do you actually keep watching — and built the interest graph instead, a feed personalized from behavior rather than relationships. A creator with zero followers could reach a million strangers overnight, because the algorithm was testing content, not networks. That single architectural choice reorganized the entire social media industry. Instagram built Reels. YouTube built Shorts. Snapchat built Spotlight. Facebook folded Reels into its main feed. None of these were coincidences. They were the industry’s largest players scrambling to copy an idea that had, without asking permission, made their existing model look slow.

TikTok also normalized something that matters enormously for this essay: buying inside social content, without leaving the feed, guided by a creator’s demonstrated taste rather than a search term you had to already know. Live shopping, product tagging inside video, the entire social commerce wave — all of it runs on rails TikTok built. That is the real Chinese export. Not a super-app. A new relationship between attention and action, one where desire and purchase sit inside the same continuous moment instead of two separate destinations connected by a search box.

Vibe shopping is the next step along that same road, not a different road entirely. TikTok collapsed the distance between watching and wanting. Agentic commerce collapses the distance between wanting and having.

What This Means

If you run a business, a platform, or a fund, the practical implications are not abstract, and they are not five years away.

If you are a founder, stop treating “AI shopping assistant” as the category. It is a feature, not a destiny. The category is delegated commercial judgement, and the company that wins it will be trusted the way a good personal shopper is trusted — quietly, completely, and for years, not the company with the flashiest demo of a single transaction.

If you are a retailer, understand that your storefront now has two audiences, and one of them cannot be charmed. A human can be persuaded by a beautiful hero image and a confident headline. An agent checks whether your returns policy is actually as generous as your homepage claims, whether your reviews look organic, whether your stated delivery time has ever been true. Build for the audience that checks.

If you are an investor, be skeptical of the fountain and curious about the hands. The valuations built on generative output are the part most exposed to the bubble correction Alex Karp is publicly worried about. The infrastructure quietly being built by Stripe, Google, Visa, Shopify and the rest around agent-to-agent commerce is the part built to survive a correction, because it solves a problem that does not go away even if the AI hype does.

If you are a policymaker or an employer, take the anger seriously rather than treating it as a PR problem to be managed with a better speech. Eric Schmidt got booed not because his delivery was poor, but because the fear underneath the boos is legitimate. The honest answer to that fear is not reassurance. It is a genuine account of which jobs change, which disappear, and which new work agentic AI actually creates — starting with the enormous, largely unbuilt industry of making commerce, logistics and services legible to software rather than only to people.

The Lord Giveth, and the Lord Taketh Away

I have written before, in The Emperor’s New Suit, that technology has never once arrived as a pure gift. It arrives, always, as a transaction whose second half is disclosed later, in smaller print, after everyone has already signed.

Goldman Sachs’ economists insist the disruption will be temporary, that new occupations will emerge the way they always have, that six or nine percent displaced over a decade is painful but survivable, historically consistent with every prior wave of automation. I do not doubt their math. I doubt their timeline, and more importantly, I doubt whether the people being displaced this decade will feel especially comforted by a labor market that heals, on average, sometime in the 2030s, for someone else’s children.

This is why the anger is not irrational, and why I think it deserves to be taken more seriously than a management consultant’s slide about “reskilling” ever will. When students at the University of Arizona booed a former Google chief executive for framing artificial intelligence as a rocket ship they should simply climb aboard, they were not rejecting technology itself. They were rejecting the specific and by-now-familiar experience of being told, cheerfully, by someone with none of their exposure and all of the technology’s upside, that the machine coming for their entry-level job is actually wonderful news. There is a very old, very human logic operating underneath every one of those boos, and it deserves to be named plainly: if the machine fails, badly enough and publicly enough, then the jobs survive, the careers survive, the future survives in something resembling its previously advertised shape. The hope that AI turns out to be a bubble is not, for most people voicing it, a financial position. It is a plea for continuity, dressed up as a market opinion.

Citrini’s report understood this instinct better than most of the industry it described, because it took the fear seriously enough to model it rather than dismiss it. Its warning was never really about the stock market, however many headlines led with the S&P number. Its warning was that a technology can work exactly as advertised — faster, cheaper, tireless, uncomplaining — and still produce a civilization-level problem, because an economy is not an engineering benchmark. It is a circulatory system, and circulatory systems do not care how efficient the heart has become if the blood stops reaching the fingers.

None of this means the technology should be strangled in its crib, and I do not believe that, any more than the loom should have been burned or the cotton gin buried. It means the second half of the transaction is coming, it is not optional, and the people building this future have a shrinking window in which to decide whether they intend to share the surplus or simply harvest it. Agentic AI will, in the fullness of time, book your travel, manage your inbox, negotiate your bills, and quite possibly write the very paragraph replacing the job of the person who would once have written it. It will give you back hours you did not know you were losing. It will also, with the same hand, take something from the people whose labor those hours used to require, and pretending otherwise is not optimism. It is simply the oldest and least convincing form of marketing there is.

The Word That Changes Everything

Sean Parker was right about “the.” Removing a word turned a college directory into a civilization.

Adding a word does the same work here, just in reverse. Software is eating the world, autonomously — and the fifteen years of sequels to Andreessen’s original essay were all describing appetite, when the real story was always going to be about who is holding the fork. For most of the internet’s history, a human held it. Every click, every search, every comparison, every abandoned basket was a person doing the work of translating desire into action.

That is ending, unevenly, industry by industry, starting with the one nobody expected: not the office, not the codebase, but the shopping cart. Vibe coding proved AI could build. Vibe shopping will prove, to a much larger and much less forgiving audience, that the machine can care — or at least behave convincingly enough like it does that the difference stops mattering to the person finally getting their evening back.

The killer app was never going to announce itself with a keynote. It was going to arrive disguised as a lobster, an errand, a boring reorder nobody wanted to do, quietly removing itself from your to-do list before you noticed it was gone.

Simba Mudonzvo is a digital marketing consultant, author, and framework builder whose work sits at the intersection of technology, commerce, and consumer behavior. Over an eighteen-year career, he has moved between insurance, big tech marketing, and digital strategy — a path that shaped his instinct for spotting structural shifts before they become obvious.

He began his career in Guernsey, spending three years in Generational Aviation & Aerospace at XL Catlin before becoming a Manager in Captive Insurance Management at Willis Towers Watson. In 2014 he returned to London to work in consulting at Marsh & McLennan, focusing on insurance and risk management. From 2015 to 2017, he served as Product Marketing Manager at ASUS, where he was product manager and media buyer on a $25 million UK budget and led the award-winning “Can You Hold Your Laptop Like This?” campaign. He studied Information Systems and Management (BSc) at Birkbeck, University of London, after an earlier stint in law school. He is the creator of several proprietary strategic frameworks, including Simba’s Five Forces, Simba’s Content Matrix, Internet Presence Optimization (IPO), Customer Ikigai, and Content/Market Fit. He is the author of seven books, including Pied Piper of Digital Marketing, The Gilded Cage, The Emperor’s New Suit, and Marketing 2030: The Future of Marketing When Customers No Longer Shop Alone.

This essay is the trailer. The report — Everything Becomes Shoppable — is the map of the territory this piece only sketched.

The essay told you agentic commerce is coming. The report tells you exactly where to stand when it arrives.